Who We Are

1STOPXBRL Limited became one of the first companies to be officially recognised by the HMRC as a provider of Managed Tagging Services back in 2010. Since then, we’ve been a trusted global provider of time sensitive financial documents.

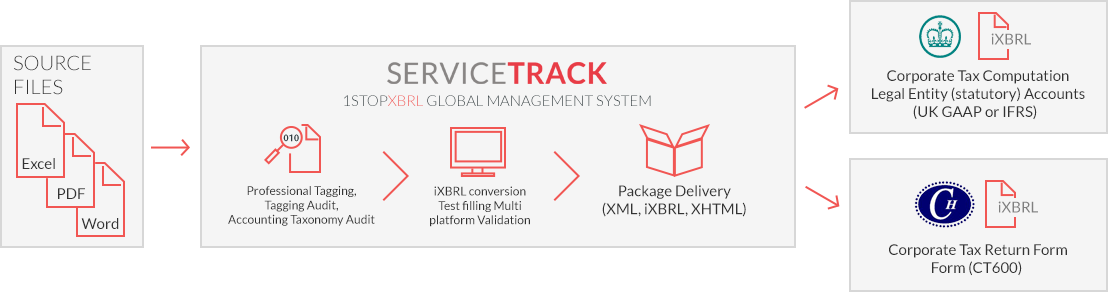

iXBRL Conversion

We prepare and convert statutory accounts and tax calculations into iXBRL instance documents ready for filing to the HMRC and Companies House.

1STOPXBRL provides you with a simple and secure gateway into our unique and proven workflow system. Our technology and quality assurance processes ensure that your output is 100% correct each and every time.

iXBRL Control System

You have free access to 1STOPXBRL`s unique iXBRL control system. This manages your iXBRL workflow, making sure you have a full audit trail of all your iXBRL documents and changes.